Balanced conditions in the city, except for apartment-style units.

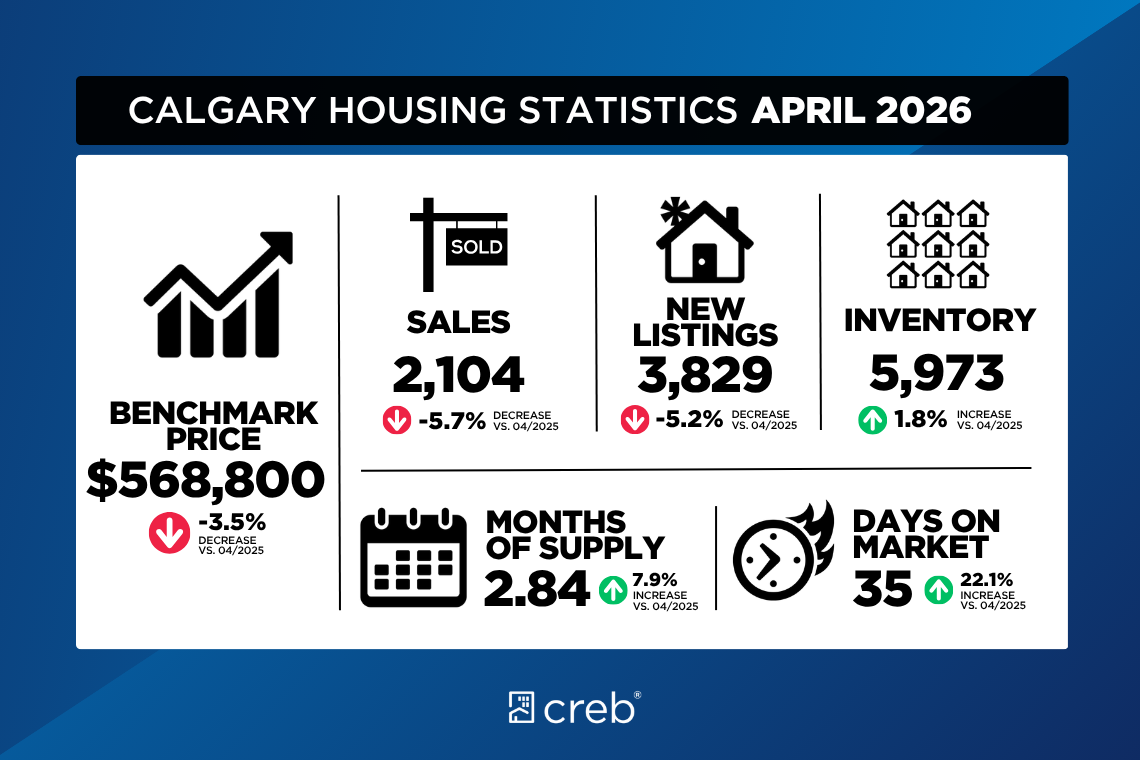

In line with seasonal expectations, both sales and inventory levels trended up relative to March’s activity. Despite this typical monthly rise, April sales totalled 2,104 units, 6% lower than levels reported in 2025.

“Sales were expected to ease this year as our market transitioned away from strong demand that was driven by previously rapid migration growth. Improved supply choice across the entire housing spectrum has reduced the urgency among potential purchasers, helping our market shift away from seller’s market conditions to more balanced conditions,” said Ann-Marie Lurie, CREB®’s Chief Economist. “However, the trend of limited supply choice in the detached market continues, while conditions favour the buyer in the apartment condominium market.”

With 3,829 new listings in April, the sales-to-new-listings ratio remained at 55%, supporting a modest monthly gain in supply. Inventory levels reached 5,973 units, nearly 2% higher than levels reported last April. Overall, the months of supply remained just below three, representing relatively balanced conditions. However, this ranged from just over two months for detached homes to over four months for apartment-style homes.

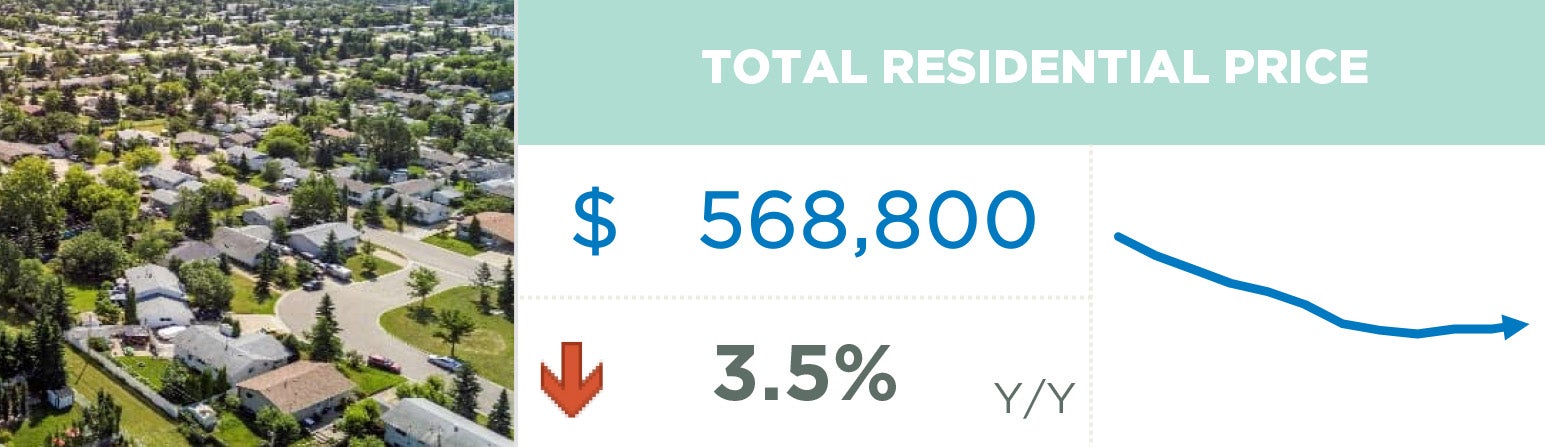

The unadjusted total residential benchmark price trended up compared with March, reaching $568,800. The monthly gain was mostly associated with seasonal improvements, which is expected heading into the spring market. Monthly gains were higher in the detached and semi-detached segments. Overall, compared with the previous year, prices remain 3% lower, with modest year-over-year declines in the detached and semi-detached sector, while declines neared 9% for apartment-style units.

So far in 2026, conditions have varied, ranging from seller’s market conditions and price growth for detached homes in some parts of the city to buyer’s market conditions and price adjustments in the apartment condominium sector.

Housing Market Facts

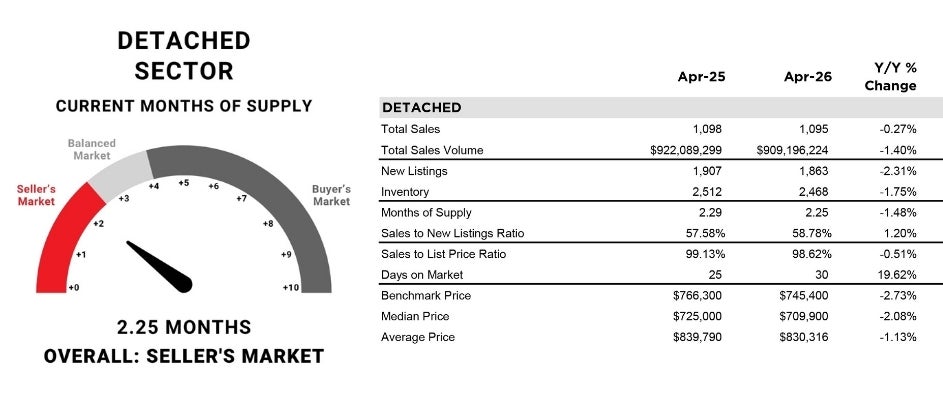

DETACHED

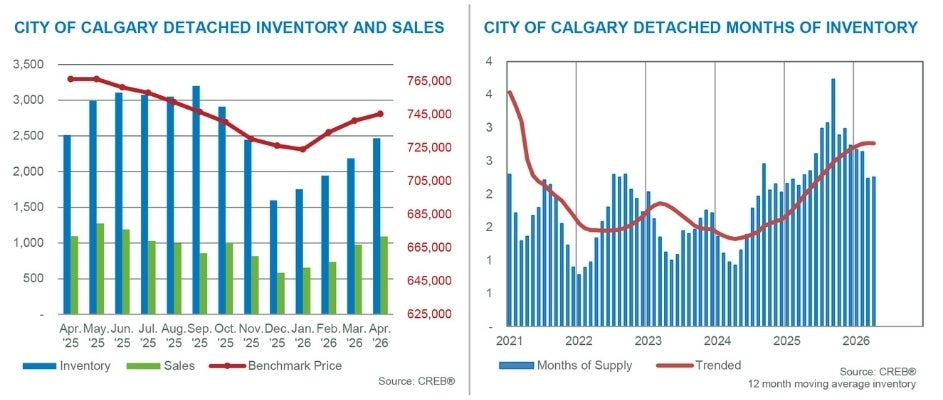

With 1,095 sales and 1,863 new listings, inventory levels reported a modest monthly gain. However, with 2,468 units in inventory, levels remain lower than those reported last year and below long-term trends, while months of supply remained just over two. The tighter conditions helped support prices in April, which continued to rise compared with March, causing the pace of year-over-year price declines to ease to under 3%. As of April, the unadjusted benchmark price was $745,400. Within the detached market, conditions varied by district. Calgary’s North West, West and South districts experienced seller’s market conditions, with less than two months of supply, driving stronger monthly price gains. Meanwhile, conditions in the North East favoured the buyer, causing prices to trend down from the previous month. Benchmark price changes in April ranged from a year-over-year decline of 8% in the North East to a 2% increase in the West district.

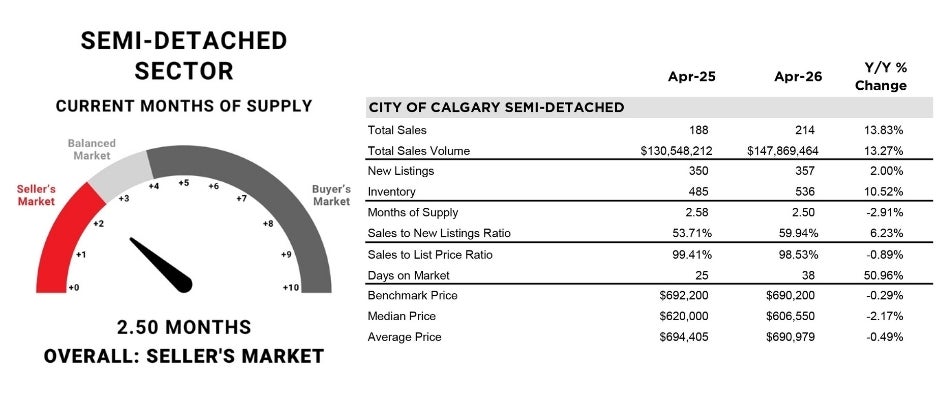

SEMI-DETACHED

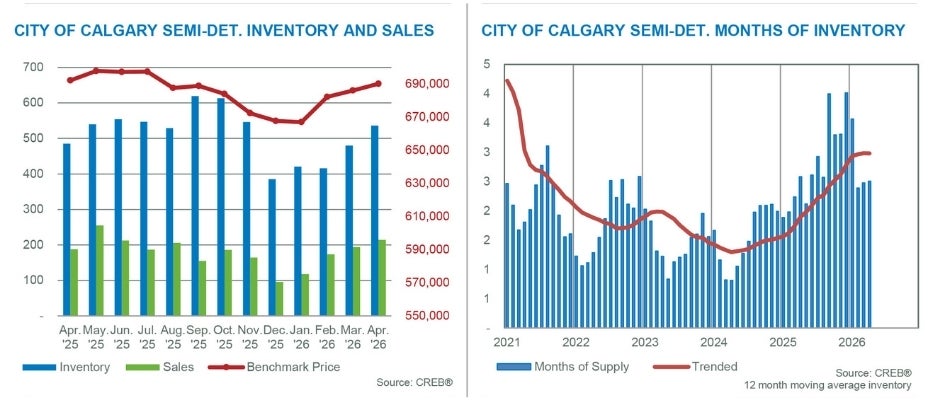

Recent improvements in new listings helped to support the rise in sales this month. Year to date, there have been 700 sales and 1,190 new listings, similar to last year’s levels. In April, both the sales-to-new-listings ratio and months of supply remained at the lower end of the balanced range. Conditions supported further monthly price growth, as the unadjusted benchmark price reached $690,000. Gains over the past three months have brought prices to levels only slightly lower than those reported last April. As in the detached sector, conditions vary by location. In April, prices trended up over March in all districts except the North East and East, which are also reporting higher months of supply. Tighter conditions in other areas supported monthly price gains. Year to date, benchmark prices improved over last year’s levels in the City Centre, North West and West districts.

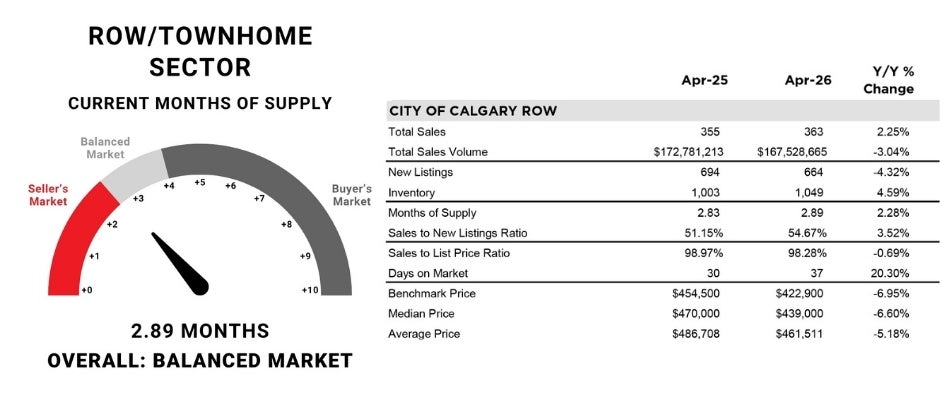

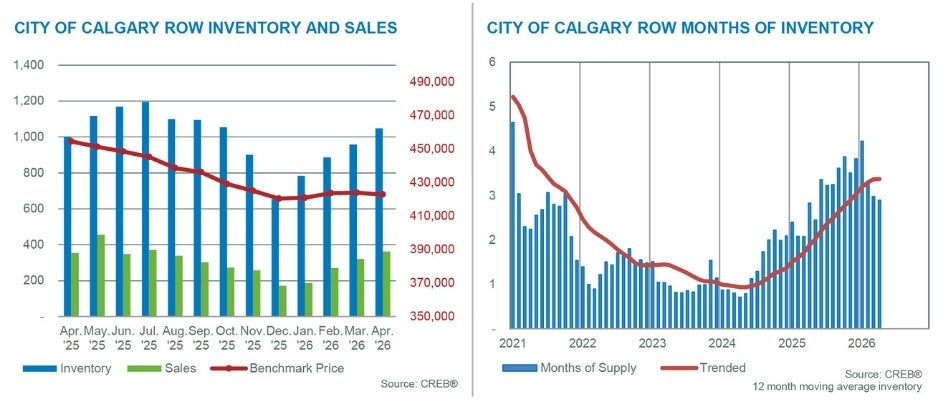

TOWNHOME/ROW

Sales, new listings and inventory levels all trended over the previous month, in line with seasonal expectations. However, year to date, the pullback in sales has outpaced the pullback in new listings, causing the sales-to-new-listings ratio to average 51% and inventories to trend higher than levels reported last year at this time. While inventories have improved, months of supply has remained in a relatively balanced range at nearly three months. Conditions vary significantly across the city, contributing to differing price trends. The North East district reported the highest months of supply and the steepest year-to-date price adjustments, at over 11%. Meanwhile, the smallest year-to-date price adjustments occurred in the West, at less than a 2% decline.

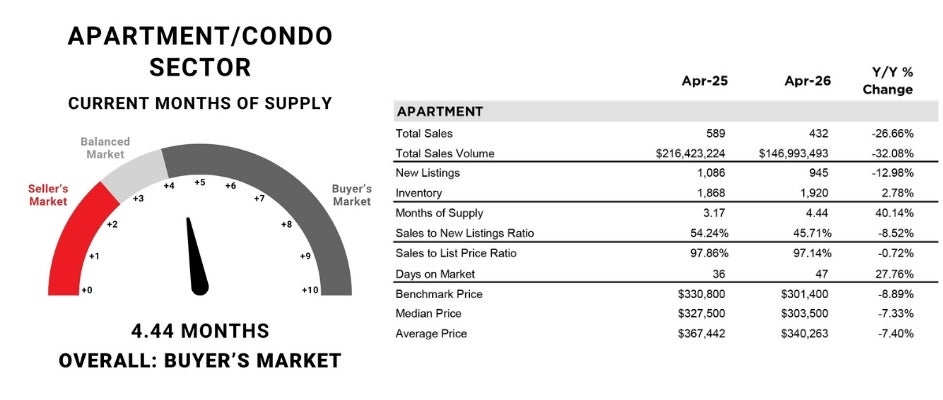

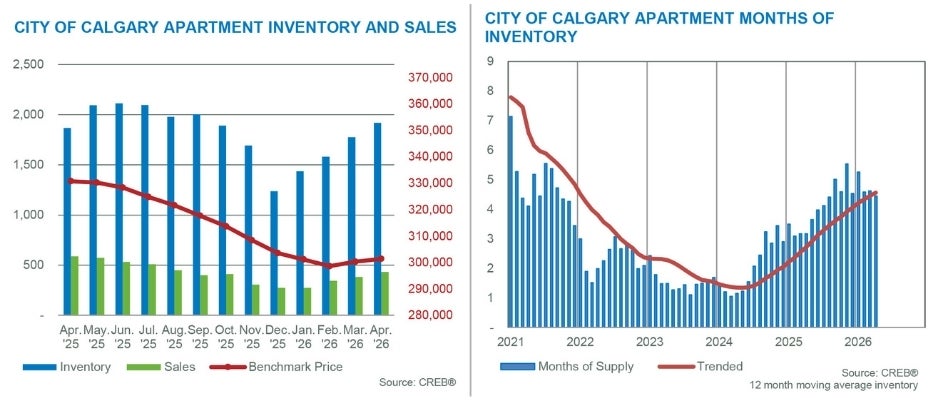

APARTMENT

The pace of growth in new listings slowed in April relative to the gains in sales, causing the sales-to-new-listings ratio to improve to 46%. However, this is not enough to prevent further inventory gains. In April, inventory rose to 1,920 units, nearly 3% higher than last year and 27% above long-term trends. With over four months of supply, conditions continue to favour the buyer, preventing any significant upward pressure on prices. As of April, the unadjusted benchmark price was $301,400, slightly higher than March. Gains were mostly driven by improvements in the North West, South East and West districts, while prices continued to trend down in the North East, North and East districts. Compared with last April, benchmark prices have declined by nearly nine per cent, with the steepest declines in the North East, East, North and South East districts.