2025 was another interesting year for the Calgary real estate market, with an overall market slowdown, though variation depended on property type, price point, and location. Certain locations and property types have seen up to a 15% decline in market value through 2025, while others have remained relatively unchanged or even gone up in value. As always, real estate values are incredibly localized.

Another major event on our radar is the upcoming public hearing on March 23rd regarding the proposed reversal of the blanket rezoning, which took effect in August 2024. If the repeal of the blanket rezoning passes, zoning will revert to what it was before the rezoning took effect. Depending on the property type, lot size, and location, this could have a positive or negative effect on sales options and market value, as zoning affects development options within a community. We hope to know more by the end of March or early April. As always, we will continue to keep you informed.

- Frances, Thomas, & Team

CREB 2025 FORECAST REPORT

Courtesy of the Calgary Real Estate Board (CREB)

ECONOMIC SUMMARY

The economy in 2025 performed better than expected, though regional differences persisted, especially in provinces affected by U.S. trade policies. Alberta and Saskatchewan, leading in growth, may benefit from regulatory reversals. However, the benefits of rising energy investments likely won't materialize in 2026 due to weaker energy prices.

In the meantime, we continue to benefit from investment in petrochemicals, hydrogen, food processing, tech, critical minerals and aviation. While relative affordability remains a benefit for our province, migration to Calgary is expected to slow as unemployment rates remain elevated. With inflation returning to target levels, the Bank of Canada is likely done cutting rates in 2026, but previous increases in the cost of living will continue to weigh on consumers.

POPULATION

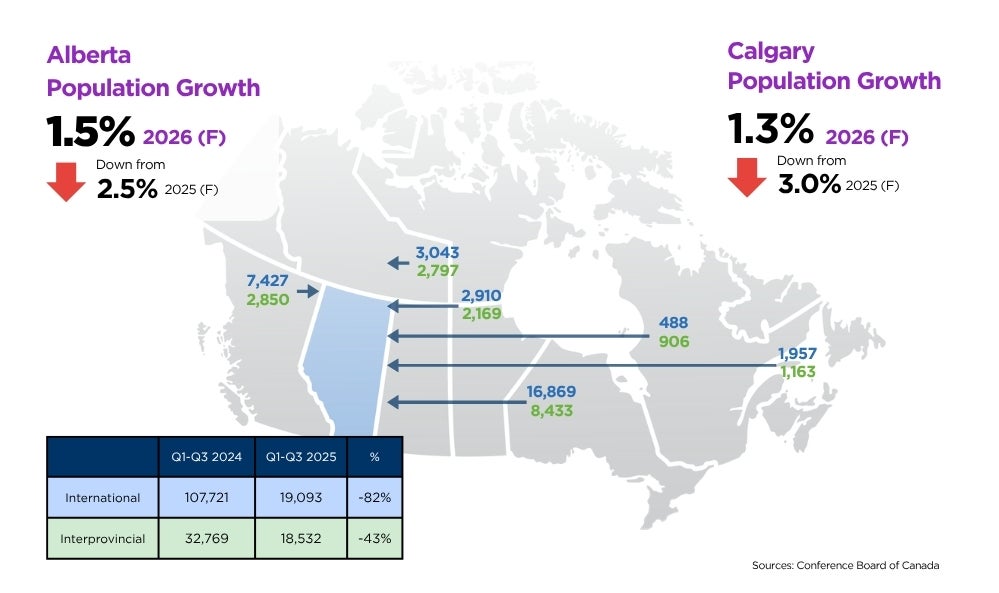

Population growth from 2022 to 2024 fueled housing supply challenges. 2025 estimates indicate a larger-than-expected decline in the number of migrants. In 2026, migration should further ease as more temporary migrants leave and fewer international arrivals occur. Interprovincial migration is also expected to slow due to weak employment and high unemployment in Calgary.

Lower migration levels are occurring as supply rises, impacting the local housing market in 2026. Although migration has slowed, it’s not as pronounced as before the pandemic, when more people left Alberta than moved in. The current shift is expected to offset long-term housing demand trends.

EMPLOYMENT

In 2025, the city’s employment grew by 4%, surpassing expectations despite declines in accommodation and food services, manufacturing, and other sectors. Growth was primarily in healthcare, social assistance, real estate, retail, and government, driven by population growth. Unemployment stayed high as the labour force grew faster than the number of jobs created. Employment growth is predicted to slow in 2026, with declines in public administration and manufacturing balancing gains elsewhere. Labour force growth is unlikely to resume as migration slows, thereby maintaining high unemployment. Although prior employment gains will support housing demand in 2026, limited growth is expected to prevent further increases in sales.

NEW HOME STARTS

New-home starts exceeded expectations in 2025, with levels approaching another record high. As of November, starts totalled 26,439, surpassing the 2024 annual total of 24,369. Starts have been elevated since 2022, as the new-home sector responded to a supply shortage caused by a sudden increase in migration. However, as the number of migrants entering Calgary slows and segments of the market show signs of excess supply, we should begin to see a pullback in new home starts in 2026.

2025 MARKET REVIEW

Courtesy of the Calgary Real Estate Board (CREB)

CREB 2026: In 2025, the market shifted from favouring sellers to more balanced conditions, as improved supply in the new home, rental, and resale markets coincided with demand returning to more typical levels. This alleviated much of the pressure on home prices last year, particularly in the apartment and row segments.

Lower migration levels, stable employment, and interest rates are expected to prevent significant changes in demand in 2026. However, supply pressures are likely to persist, as 26,000 units currently under construction are expected to be completed over the coming years.

Much of the supply growth will be in apartment-style homes, and while starts are expected to slow in 2026, it will take time to absorb the supply, given the weaker migration levels. Ultimately, this will continue to exert downward pressure on prices for apartment- and row-style homes. Meanwhile, conditions are more balanced for detached and semi-detached homes, supporting relative price stability for those properties.

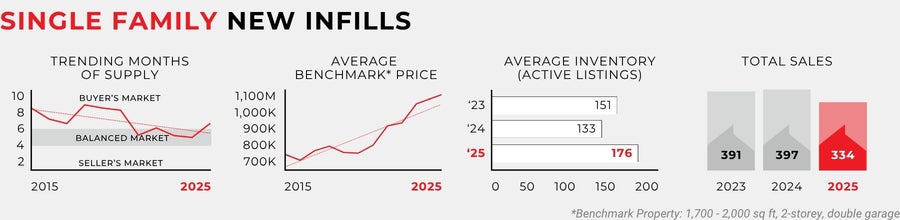

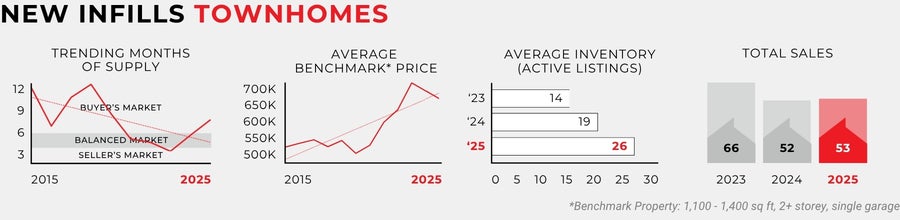

2025 NEWINFILLS MARKET REVIEW

Similar to the overall Calgary market in 2025, the new infill sector experienced a range of conditions depending on property type, location, and price point.

The single-family new infill sector ended the year with 334 sales, down 16% from its peak in 2024. Slowing sales and rising listings did impact inventory levels, which rose through 2025. Average inventories in the single family sector were 176 through 2025, the highest level since 2020. Despite the slower market, prices overall remained quite strong in the single family sector, with benchmark pricing actually rising in 2025 by 3%.

The new infill townhome sector ended the year with 53 sales, relatively unchanged from 2024. This was mostly due to rising inventory levels providing buyers with more purchasing opportunities. Rising inventories and a softer overall market did lead benchmark pricing for new infll townhomes to drop by 3% in 2025.

2026 SO FAR

The market so far in 2026 has seen a continued variance across locations and product types. Generally speaking, the market is strongest in the single-family sectors (both detached and semi-detached), where overall conditions remain fairly balanced and, in some locations, even favour the seller. The townhome market has slowed a bit, although conditions remain balanced overall. The apartment sector remains the slowest area of activity, with buyer market conditions persisting.

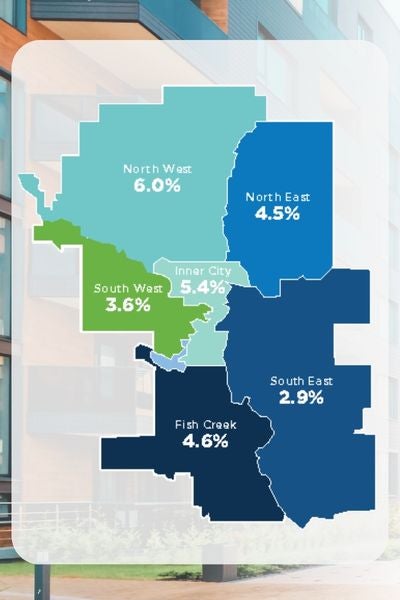

The market is also seeing a range of conditions depending on location. Some districts (like the East and North East) continue to see more significant downward price corrections, while others (like the West and City Centre) are overall fairly stable.

Looking ahead, we believe that if the blanket zoning repeal passes, the market will see adjustments both upwards and downwards, depending on property type and location, as development options change.

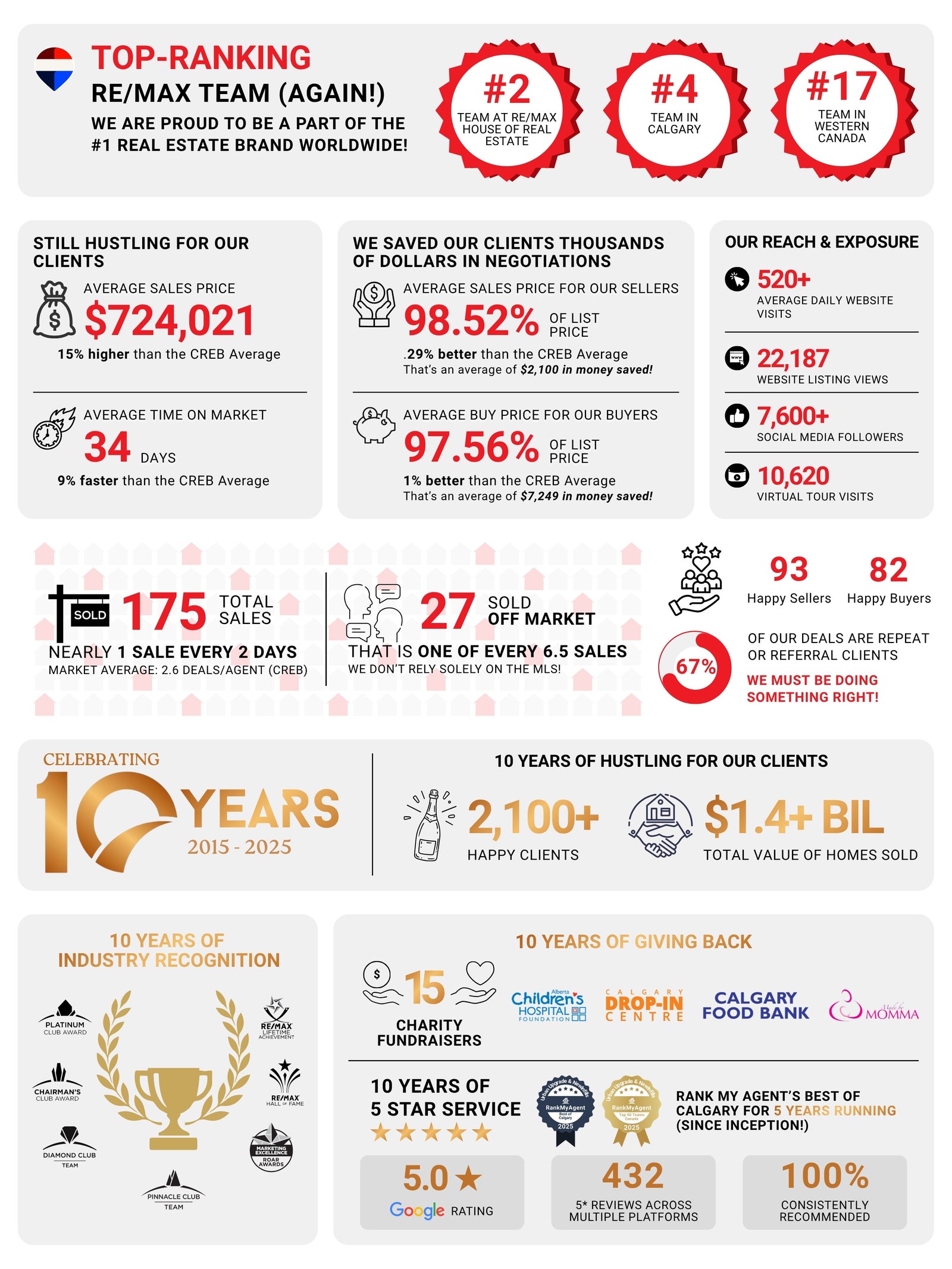

URBAN UPGRADE 2025 PERFORMANCE STATS

AGENT SPOTLIGHT

It’s time to shine the spotlight on the newest member of our Growing team...

1. Why did you get into real estate?

I love connecting with people and building lasting relationships, and that naturally ties into my genuine passion for Calgary’s constantly evolving real estate market. Watching the city grow and change inspires me and drives me to help others find their place within, fostering meaningful, long-term connections along the way.

2. What do you love most about buying and selling homes?

I love touring the city's beautiful homes and making my clients happy when they find their dream home and sell their previous home with ease.

3. What’s your #1 tip for a successful sale?

I would say it's all about pricing your home correctly; a well-priced home attracts competition and can even drive prices up. In real estate, the first impression on the market is everything.

4. What’s it like being on the Urban Upgrade & NewInfills team?

I love the team aspect and all the support I get on a day-to-day basis.

Want to learn more about our agents?

Read everyone's full bios on Our Team page!

NEWS FLASH

What Were the Key Rule Changes?

1. Broader Definition of STRs

Short-term rentals are now defined as stays of up to 180 consecutive days (previously 30). As a result, more mid-term furnished rentals now require STR licensing.

2. Mandatory Business Licence for All Hosts

Anyone offering a property for short-term stays must hold a valid City business licence, reinforcing that STRs are a regulated commercial activity.

3. Two Licence Categories Introduced

Primary Residence: The host resides in the home.

Non-Primary Residence: Investment or secondary properties operated as full-time STRs.

4. Vacancy-Rate Control Mechanism

If Calgary’s rental vacancy rate drops below 2.5%, the City can pause issuing new licences for non-primary-residence STRs to help protect the long-term rental supply.

5. Platform & Safety Requirements

Booking platforms must be licensed, and operators must meet updated safety, insurance, and documentation standards to ensure guest protection and accountability.

Sources:

CitNews Calgary - New rules for short-term rentals in Calgary take effect

WHAT'S BEING PROPOSED?

If passed, the repeal will revert zoning for residential properties to their previous state before the blanket rezoning took effect. For most inner-city areas, this means a return to a lower-density R-C1 or R-C2 zoning.

WHAT ELSE IS CHANGING?

There are also significant changes proposed to the R-CG bylaw that will affect what can be built on parcels that retain this zoning. This includes:

Townhomes are only permitted on corner lots

Density for typical lots reduced from 4 units to 3 units

HOW WILL THIS AFFECT MY PROPERTY VALUE?

This depends on location, lot size, and property type. Some properties are expected to rise in value while others are expected to fall as development options are reduced.

HOW WILL THIS AFFECT DEVELOPMENT?

Generally speaking, density should decrease in future development, and many RC-1 areas will no longer see much infill development at all.

HAS THIS BEEN APPROVED BY COUNCIL?

Not yet. A public hearing has been set for March 23, 2026. Following the hearing, the bylaw will be considered by Council. Stay informed and learn more at calgary.ca/planning/projects/rezoning]

MAKING HEADLINES

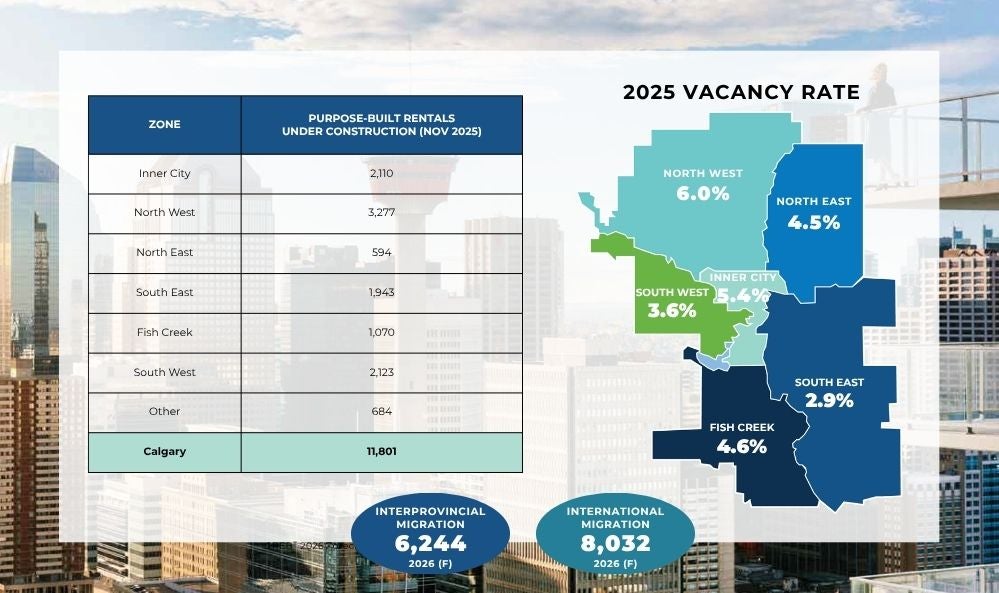

Purpose-built rental construction has surged to record levels after rental rate gains and low vacancies. However, the recent drop in international migration coincides with these units entering the market, increasing vacancy rates and pushing down rents.

Over 11,801 units are still under construction and will be completed in the coming years.

With international migration numbers expected to remain low, it will take longer for the additional supply to be absorbed. This will likely keep vacancy rates elevated in 2026, further weighing on rental rates.