Calgary continued to see market conditions vary by property type in February. The tightest conditions occurred in detached and semi-detached properties, reporting less than three months of supply. Row homes reported slightly higher supply levels relative to demand but remained relatively balanced. Meanwhile, apartment-style properties are dealing with excess supply, as conditions continue to favour the buyer.

“Slowing migration levels are coming at a time when supply for apartment-style homes is rising. Calgary reported record high starts last year, mostly due to gains in apartment starts where there are nearly 18,000 units currently under construction. While a large share of the units is targeted for rental, this also impacts condo ownership markets,” said Ann-Marie Lurie, CREB®’s Chief Economist. “Meanwhile, on the opposite end of the spectrum, the detached market remains relatively balanced in the higher price ranges and continues to struggle with limited supply for homes priced below $700,000.”

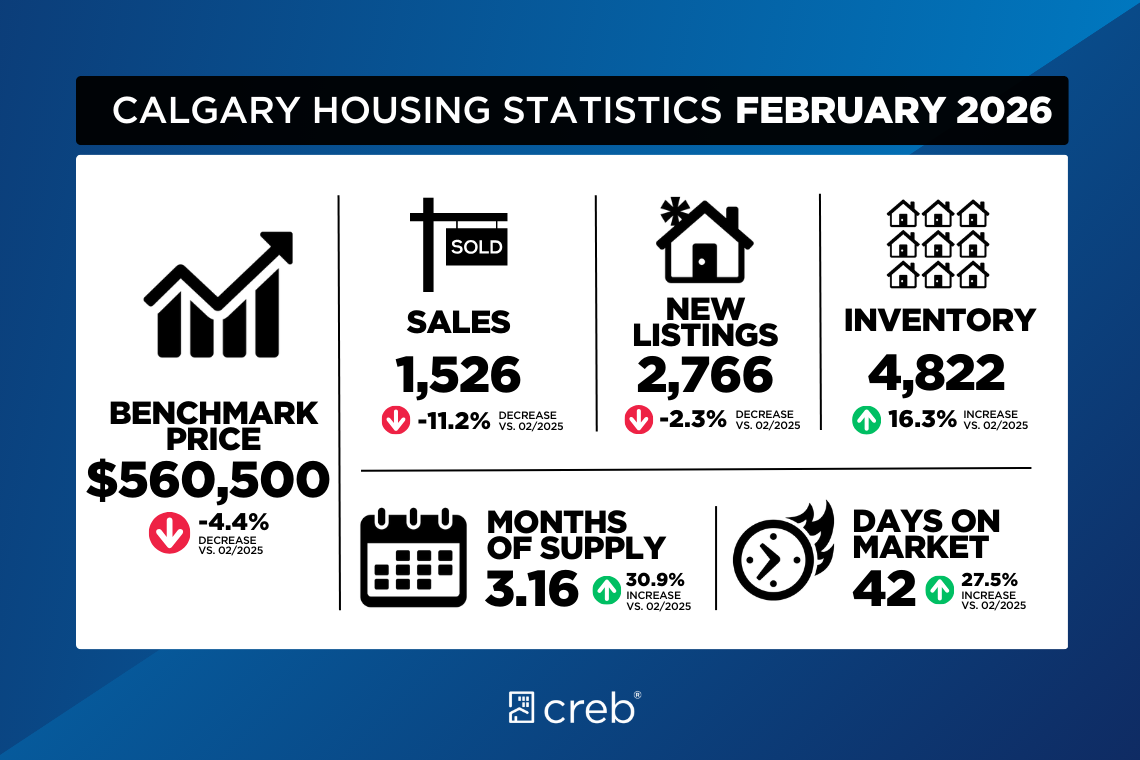

Tighter conditions for detached homes offset the higher supply levels in the apartment condominium sector, leaving citywide conditions relatively balanced at three months of supply and a sales-to-new-listings ratio of 55%. Inventory levels reached 4,822 units in February, with condominiums and row homes representing more than half of all the inventory. At the same time, there were 1,526 sales in February, an 11% decline over last February, mostly due to a sharp pullback in row and apartment sales.

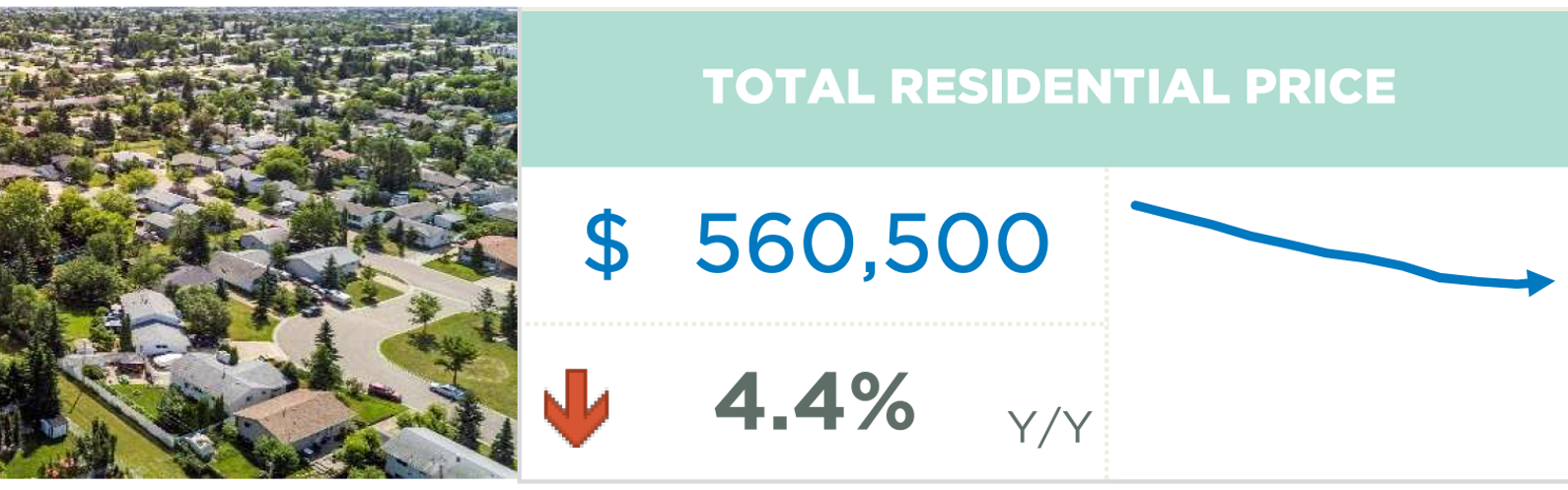

Typical seasonal patterns tend to drive monthly gains in prices early in the year following the monthly slides reported at the end of the previous year. While February did report monthly benchmark price gains for most property types, prices continued to slide for apartment-style homes. However, monthly gains for lower-density homes offset the pullbacks for apartment units, leaving the total residential benchmark price of $560,500 1% higher than January, but still 4% lower than last year's levels.

Housing Market Facts

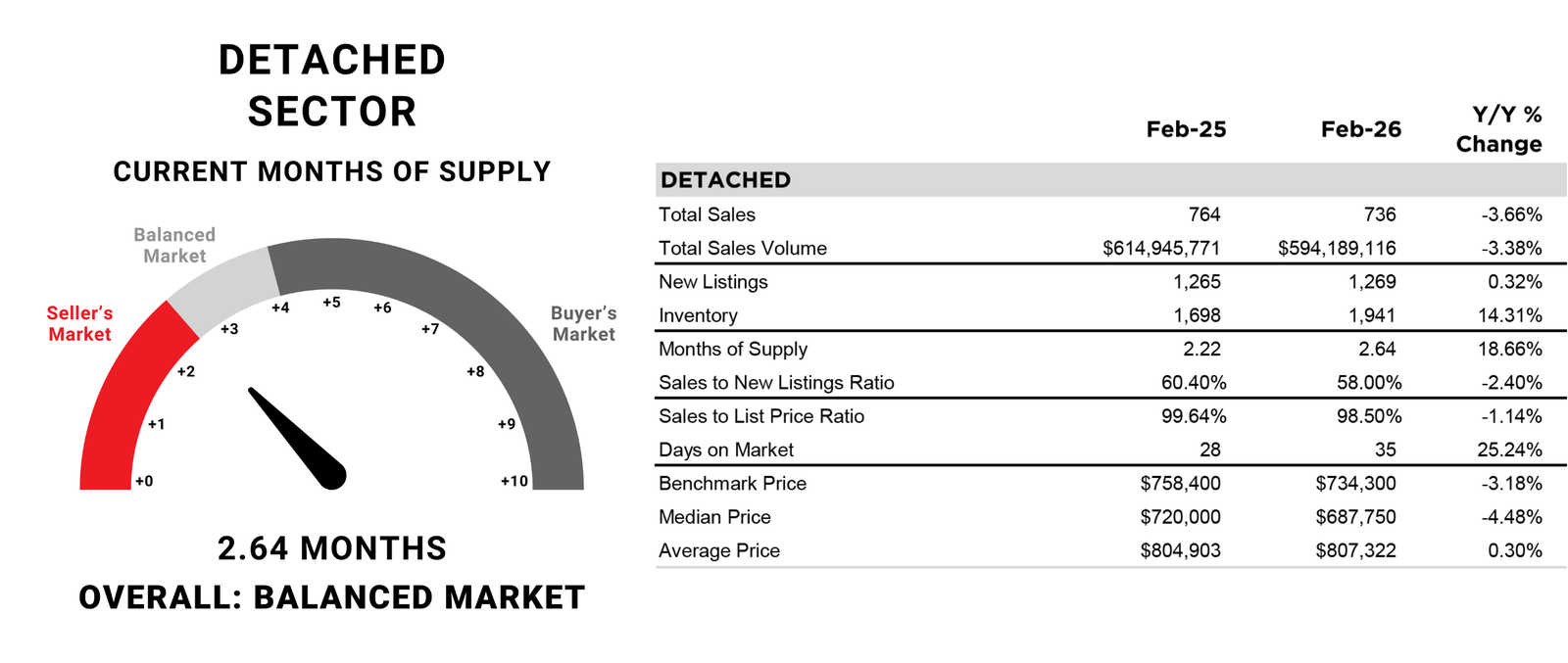

DETACHED

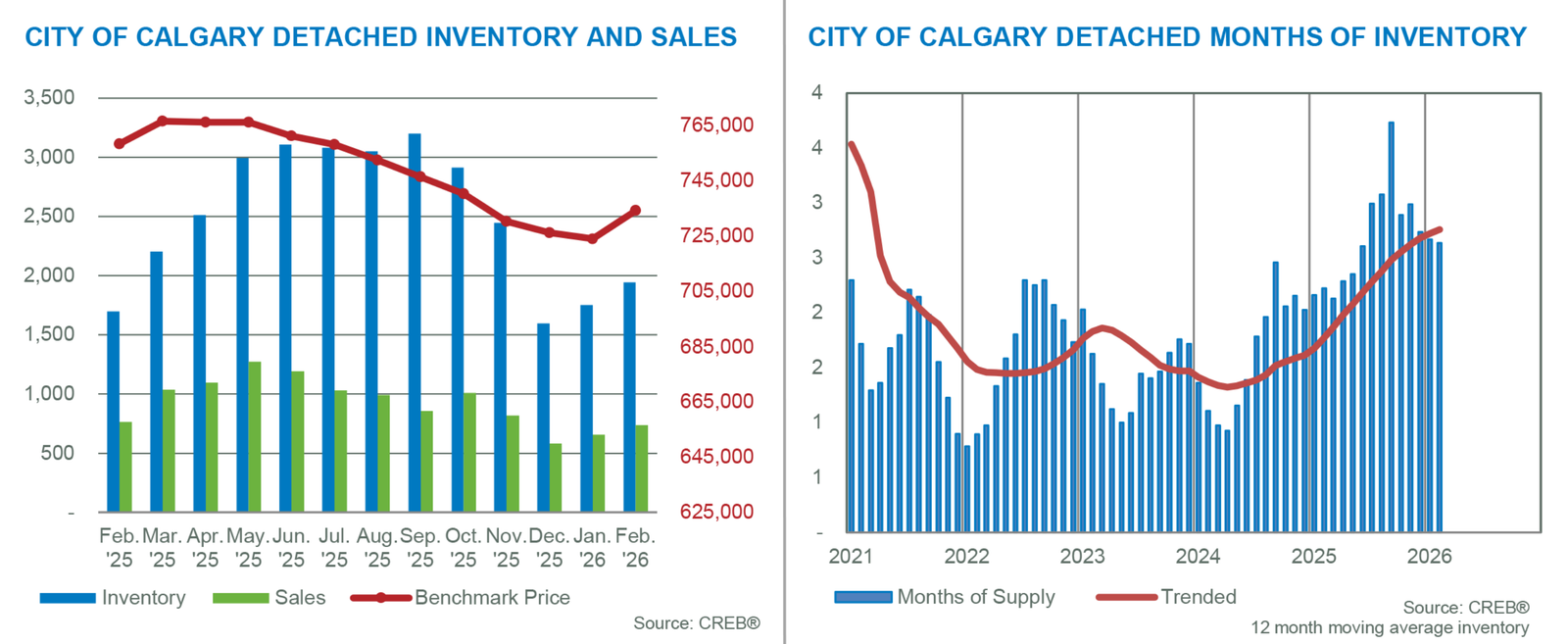

Both sales and new listings in February were similar to levels reported last year. With 736 sales and 1,269 new listings, the sales-to-new-listings ratio was 58%. While this did not prevent further inventory gains, months of supply remained relatively balanced at just under three months. Conditions did vary across the city as the North East district struggled with excess supply, preventing any improvement in monthly prices. Meanwhile, the West district reported the tightest conditions with less than two months of supply.

In February, the unadjusted benchmark price for a detached home was $734,300, over 1% higher than January, but still 3% lower than last year's levels. The only districts to report both month-over-month and year-over-year gains were the City Centre and the West district.

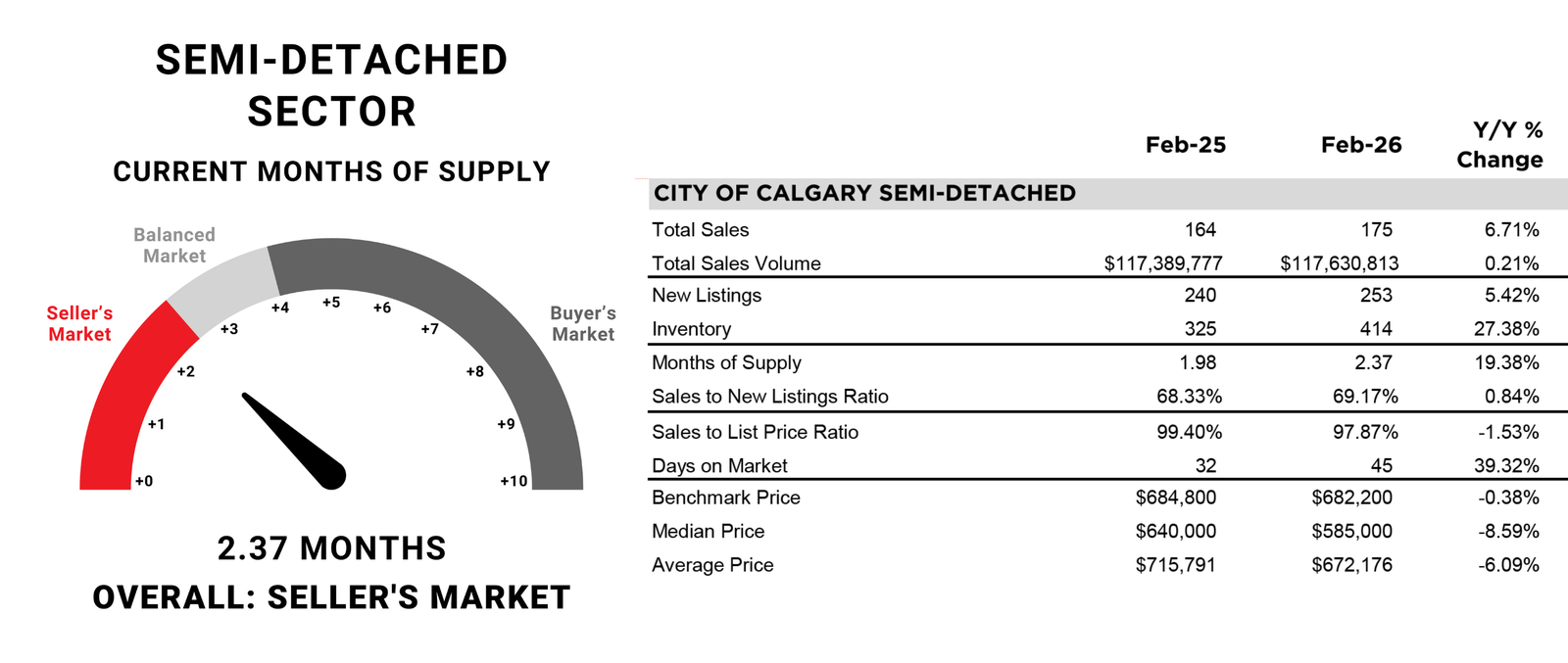

SEMI-DETACHED

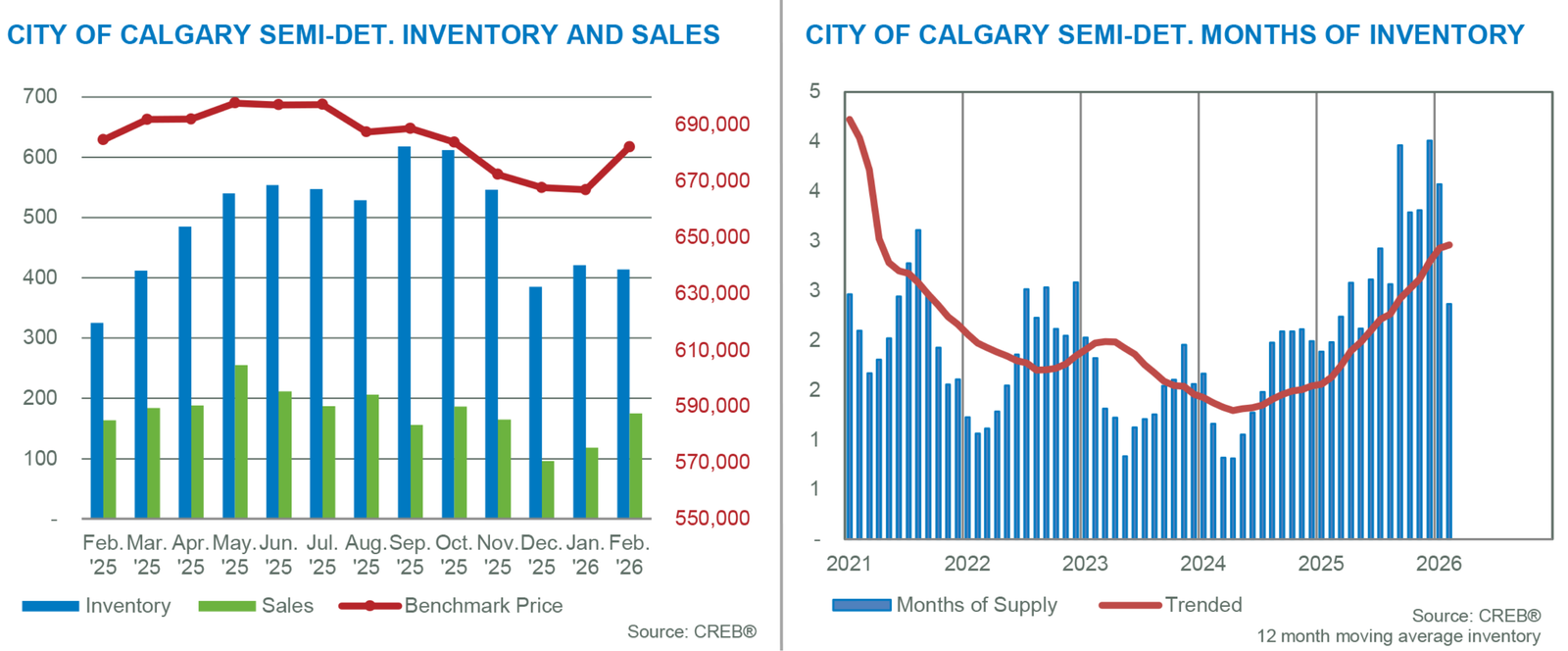

Sales improved in February, reaching 175 units. At the same time, new listings rose to 253 units, causing the sales-to-new-listings ratio to rise to 69% and preventing any improvement in inventory levels compared to January. This caused the months of supply to drop to 2.4 months, the lowest out of the four property types.

While this is a smaller segment of the market, the tighter conditions did result in slightly higher monthly price gains. As of February, the unadjusted benchmark price was $682,200, over 2% higher than January and comparable to levels reported last year. Year-over-year price changes varied by district, with gains in the City Centre, North West and West offsetting declines in the North East, North, South, South East and East. In addition to typical seasonal factors, tighter conditions at the start of the year are helping support monthly price gains in most districts.

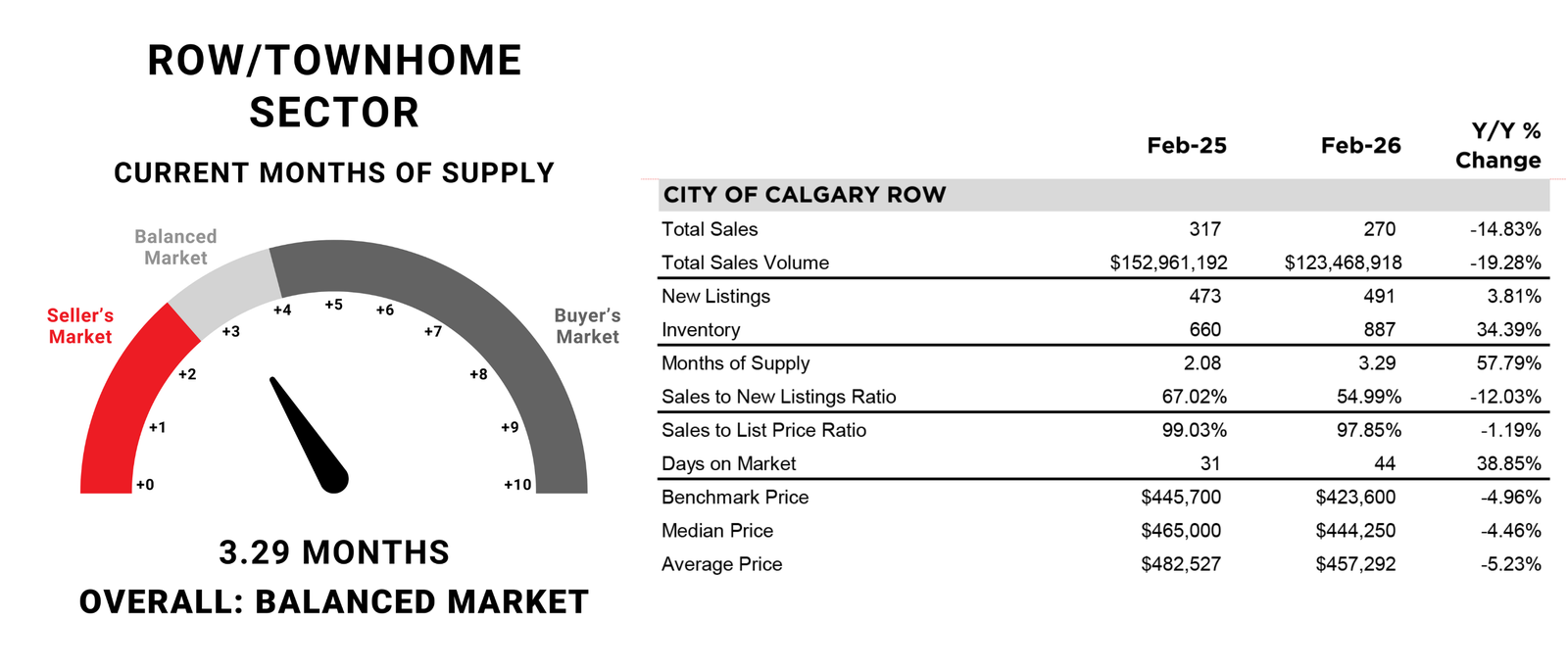

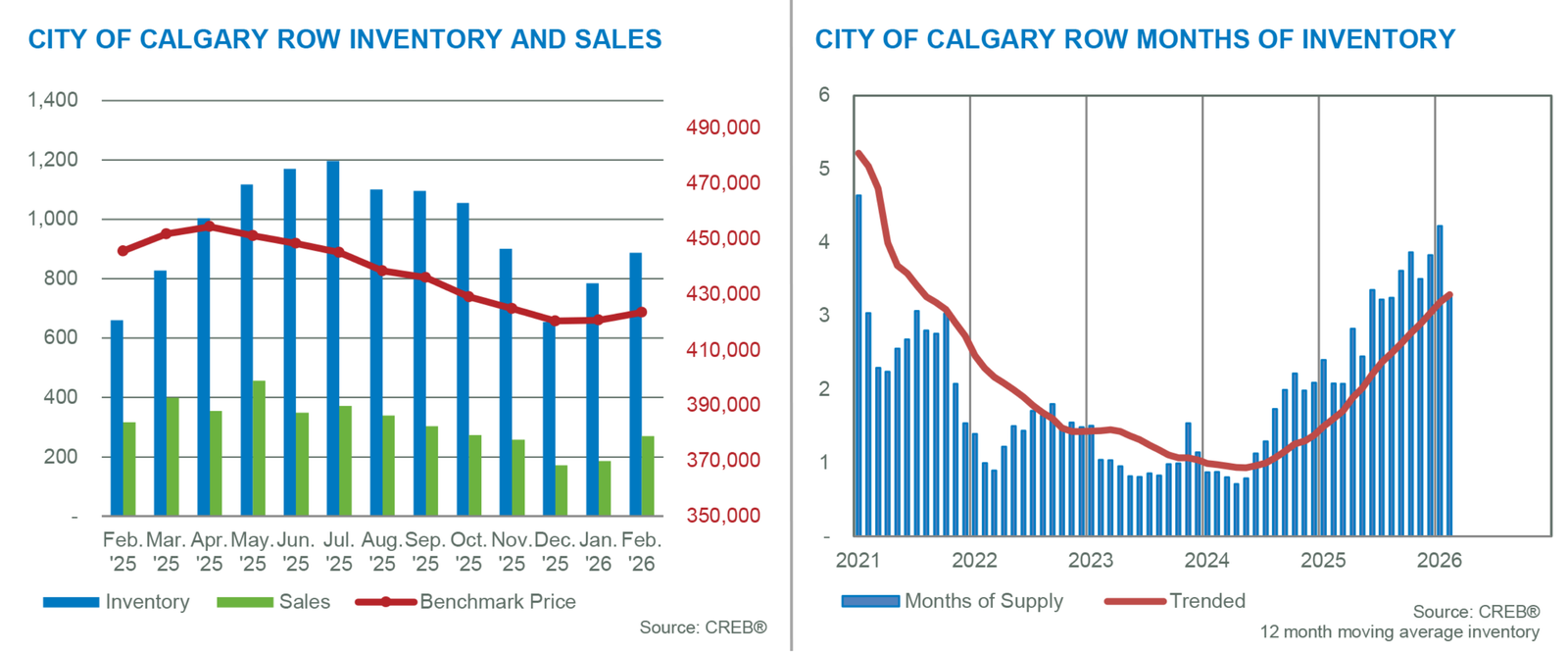

TOWNHOME/ROW

Sales picked up in February compared to January, reaching 270 units. Meanwhile, after January’s surge in new listings, levels slowed to 491 units, helping bring the sales-to-new-listings ratio into more balanced territory at 55%. While inventories did rise, the monthly gains in sales helped reduce the months of supply from over four months in January to just over three months in February.

The unadjusted benchmark price rose to $423,600 in February, in line with typical seasonal expectations. While prices are still 5% lower than last February, there is significant variation between districts. The steepest year-over-year declines have occurred in the North East and East districts at over 10%. Meanwhile, prices in both the West and City Centre are only slightly lower than levels reported last February.

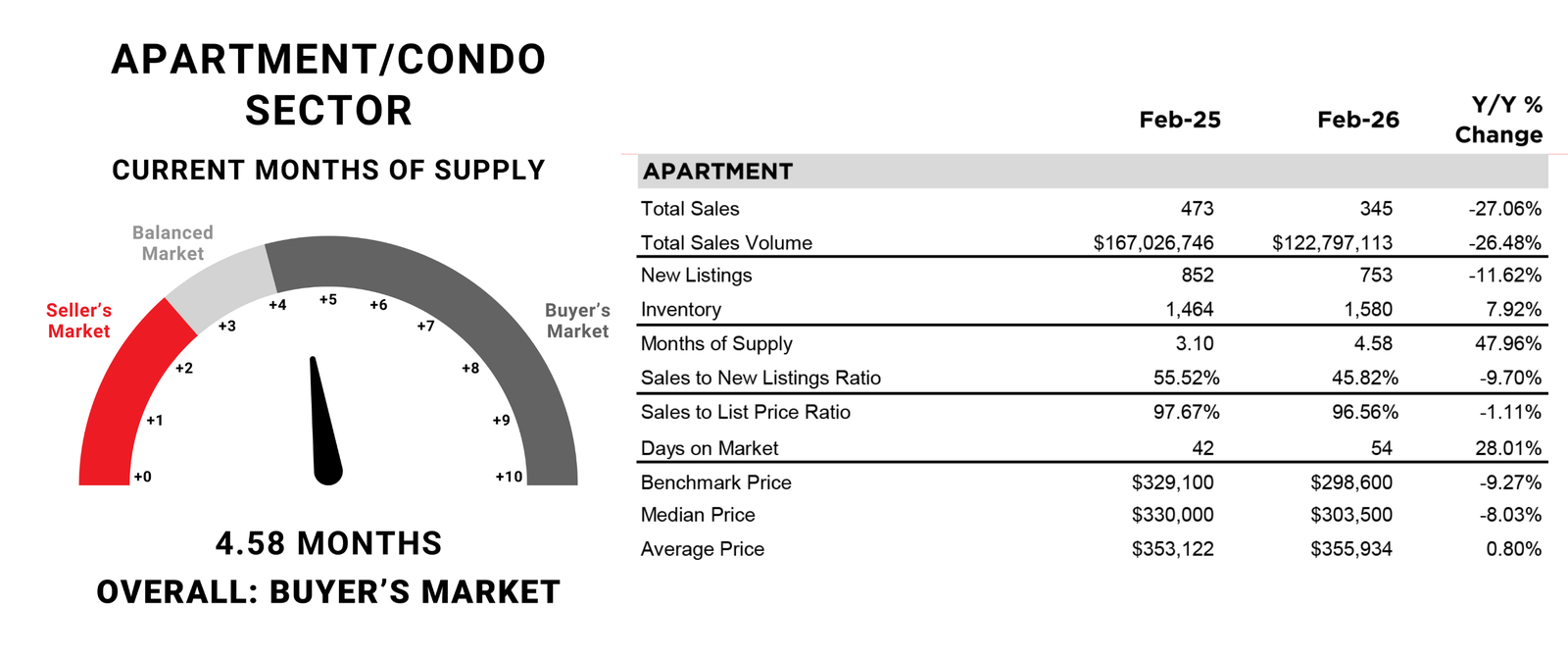

APARTMENT/CONDO

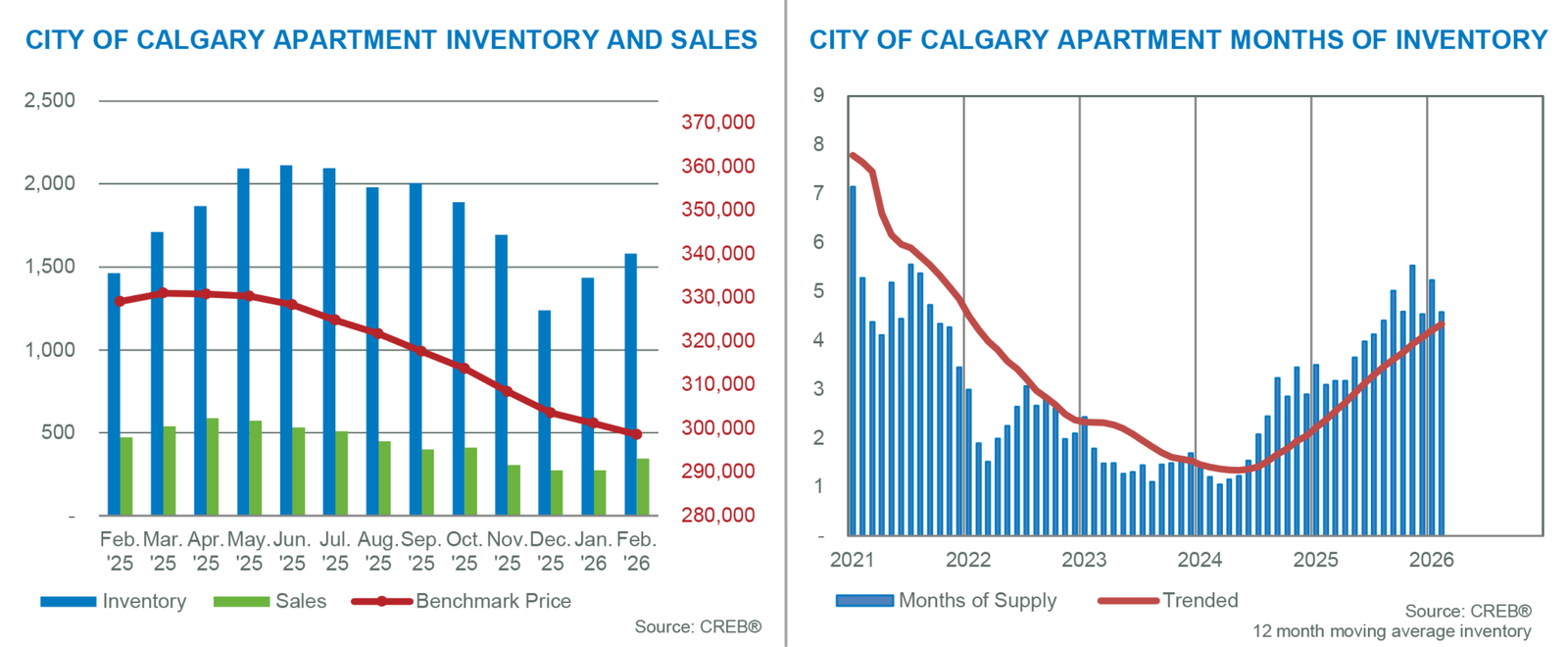

Despite a pullback in new listings in February, with 753 new listings and 345 sales, the sales-to-new-listings ratio remained low at 46%, contributing to further inventory gains. February reported 1,580 units in inventory, high enough to keep the months of supply well over four months. The persistently higher supply levels continued to weigh on prices in February, as the monthly benchmark price dropped to $298,600, nearly 1% below January and over 9% lower than prices reported last February.

Conditions do vary across the city. After the first two months of the year, the months of supply have ranged from over 11 months in the North East to below four months in the South district. The higher supply levels are weighing on prices across all districts. The largest year-over-year price adjustments have occurred in the North East, East and South East districts, which have seen declines surpassing 10%.