New listings in November reached 2,227 units, nearly 40 percent higher than the exceptionally low levels reported last year at this time. Gains in new listings occurred across most price ranges, but the most significant gains occurred from homes priced over $600,000.

Despite the year-over-year jump in new listings, inventory levels remained low thanks to relatively strong sales. With 1,787 sales in November, the sales-to-new listings ratio remained high at 80 percent, and the months of supply remained below two months.

“Like other large cities, new listings have been increasing,” said CREB® Chief Economist Ann-Marie Lurie. “However, in Calgary, the gains have not been enough to change the low inventory situation thanks to strong demand. Our market continues to favour the seller, driving further price growth.”

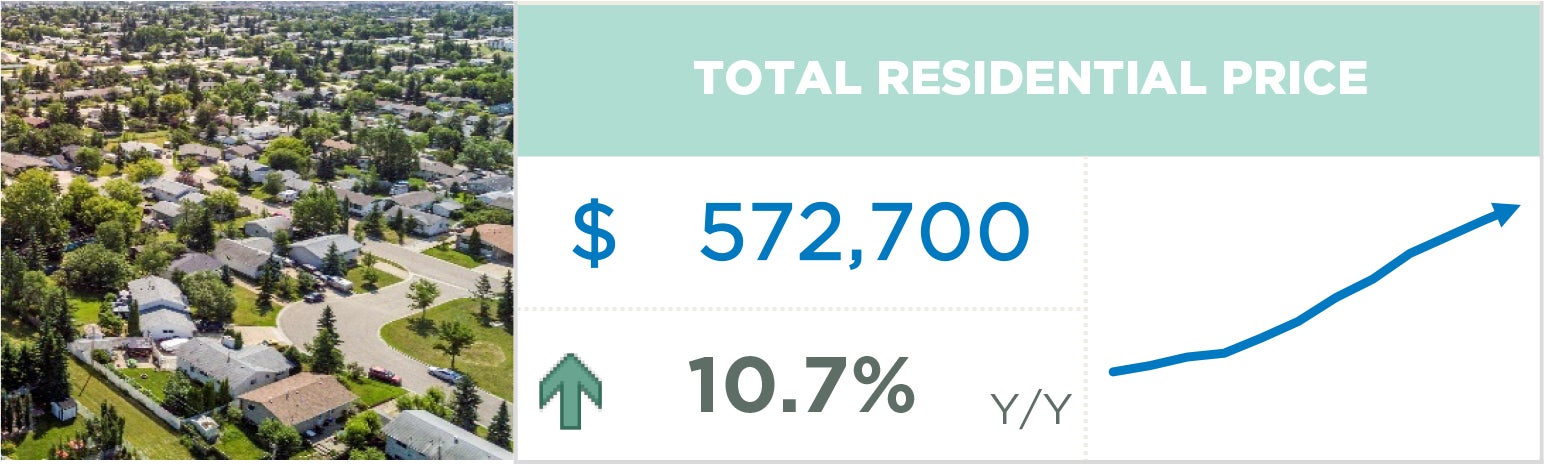

As of November, the benchmark price was $572,700, up over last month and nearly 11 percent higher than November 2022. Year-to-date, the average benchmark price has risen by over five percent.

Housing Market Facts

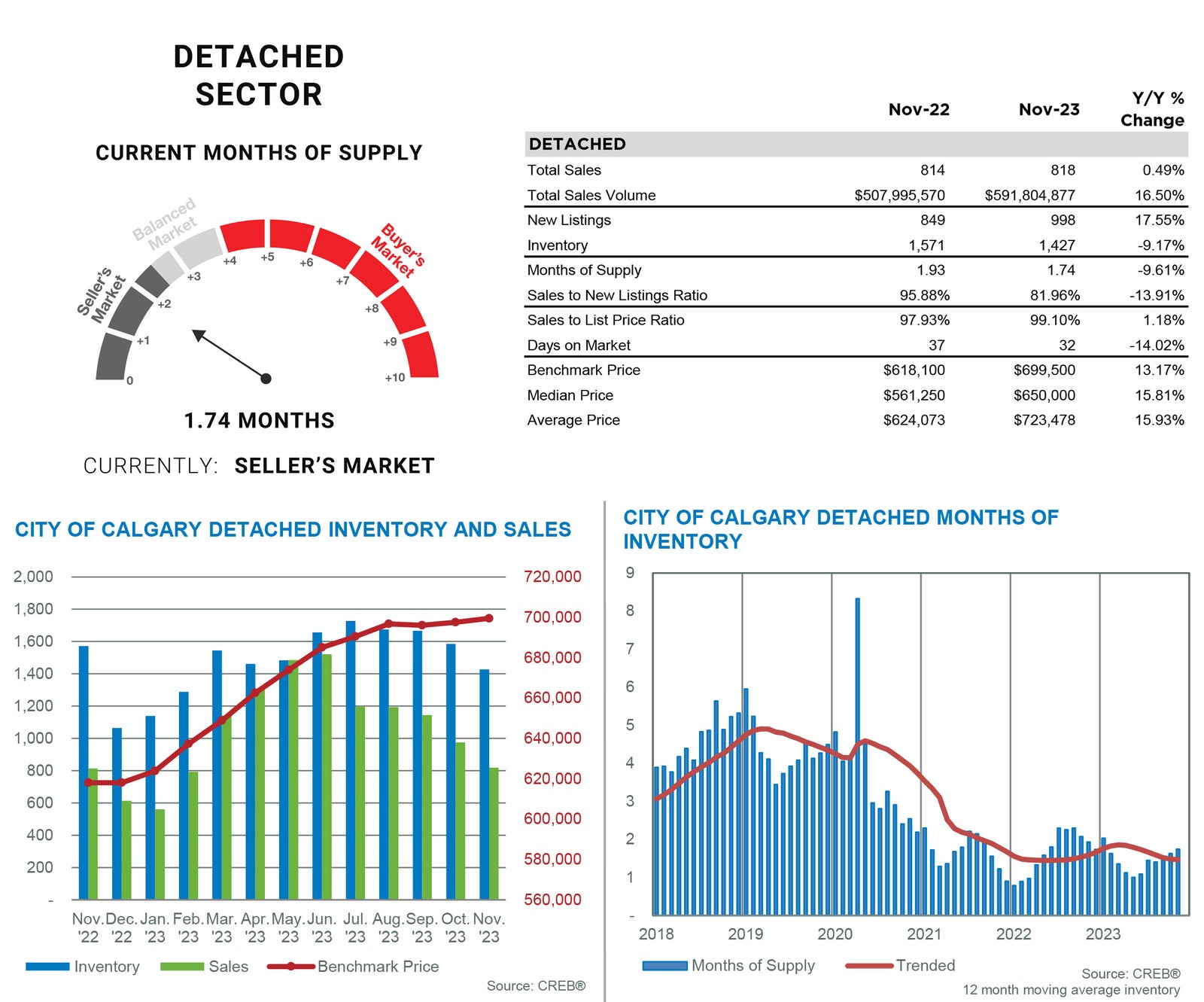

DETACHED SECTOR

Limited supply choice for homes priced below $700,000 has been the primary cause of the decline in detached home sales. While November reported a marginal gain over last year, year-to-date sales have declined by 20 percent. November saw a rise in new listings compared to the previous year, but higher-priced homes drove most gains. This has left the detached market with exceptionally tight conditions for prices below $700,000 and more balanced conditions for higher-priced homes. Overall, the month of supply remains exceptionally low at under two months.

Persistently tight conditions continue to cause further price gains in the detached market. As of November, the unadjusted benchmark price reached $699,500, a slight increase over last month and over 13 percent higher than last November. While detached home prices are much higher than last year's levels in every district, year-to-date gains are the highest in the most affordable districts of the Northeast and East.

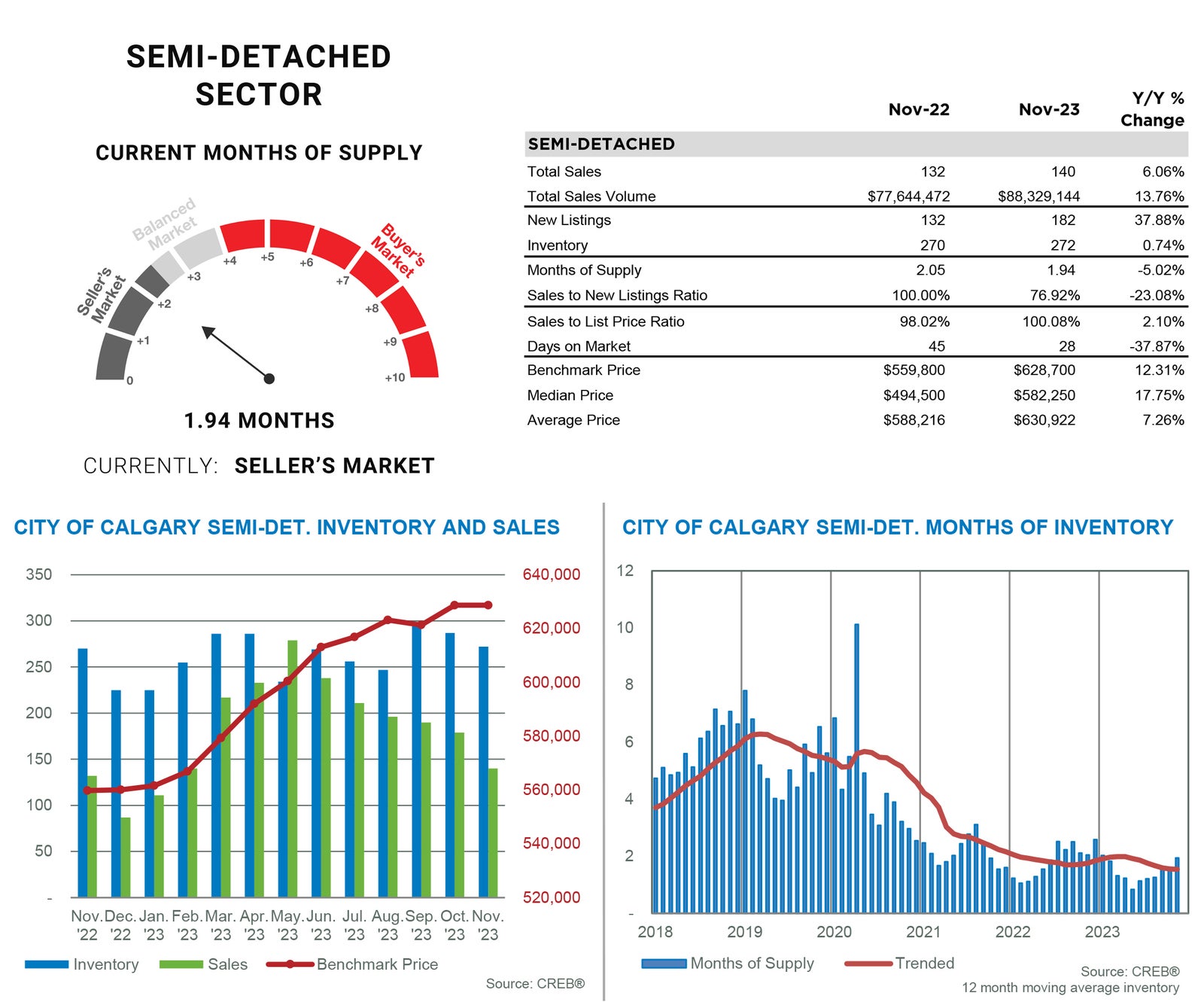

SEMI-DETACHED SECTOR

November saw a boost in new listings compared to last year, helping to prevent a year-over-year decline in inventory levels. However, inventory levels are still over 40 percent below the typical levels seen in November. With a sales-to-new-listings ratio of 77 percent and a month-of-supply below two months, conditions remain exceptionally tight, especially for homes priced below $700,000.

Despite tight conditions, benchmark prices remained stable compared to last month. However, at an unadjusted benchmark price of $628,700, prices are still over 12 percent higher than last year. The year-to-date average benchmark price has risen by nearly seven percent, with the largest gains occurring in the North East and East districts.

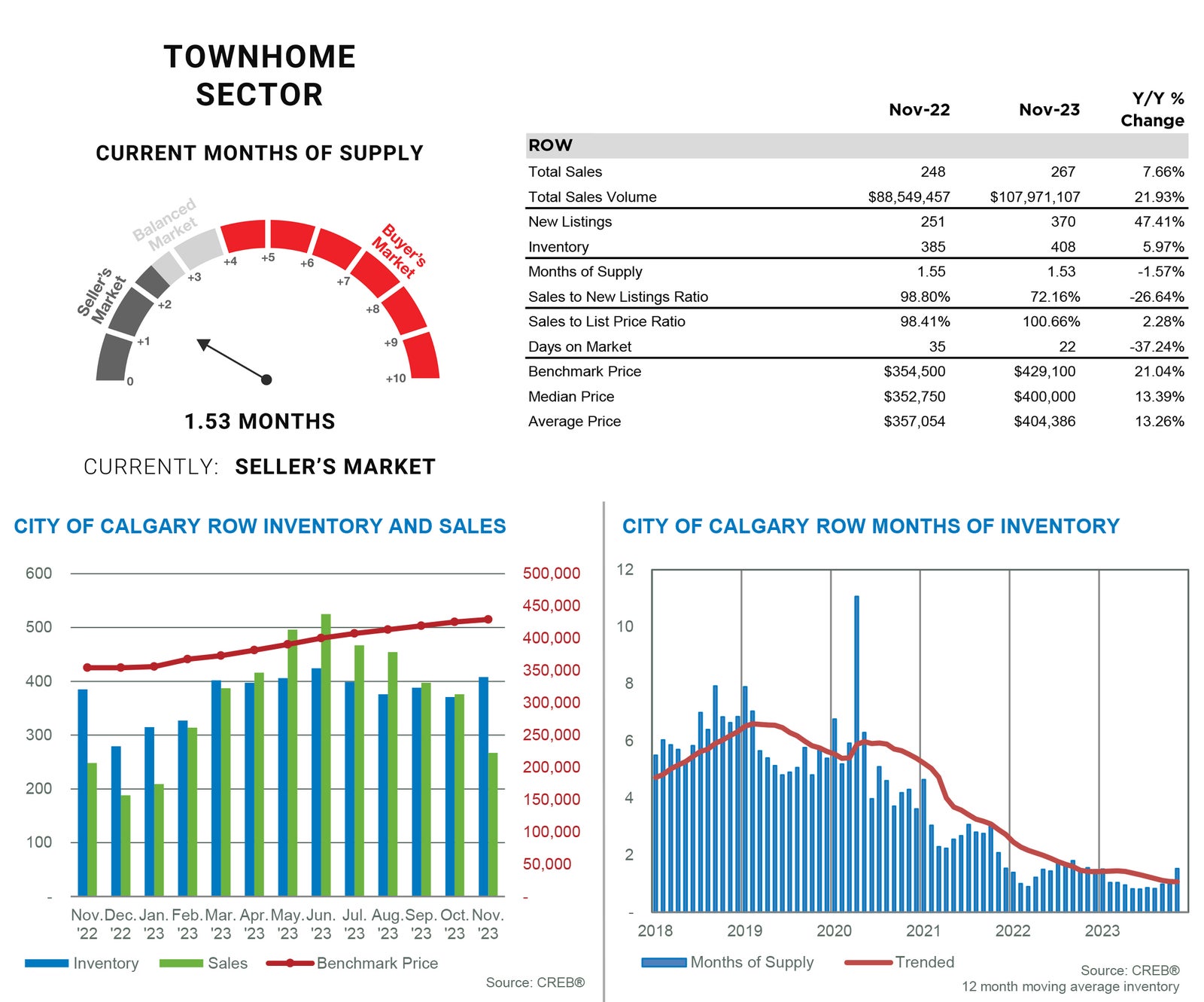

TOWNHOME SECTOR

New listings rose again this month compared to last year. The 370 new listings were met with 267 sales, and for the first time since 2021, the sales-to-new-listings ratio fell below 75 percent. The jump in new listings was enough to support a gain in inventory levels compared to last month and last year. While inventories are still nearly half the levels we traditionally see, this did help cause the months of supply to push up to 1.6 months, a significant improvement from the less than one month of supply that has persisted over the past seven months. While conditions are much more balanced in the higher price ranges, there is less than one month of supply for homes priced below $500,000.

Despite the shift away from exceptionally tight conditions, prices still rose over the last month and last year. As of November, the unadjusted benchmark price reached $429,100, 21 percent higher than last November and an average year-to-date gain of nearly 13 percent.

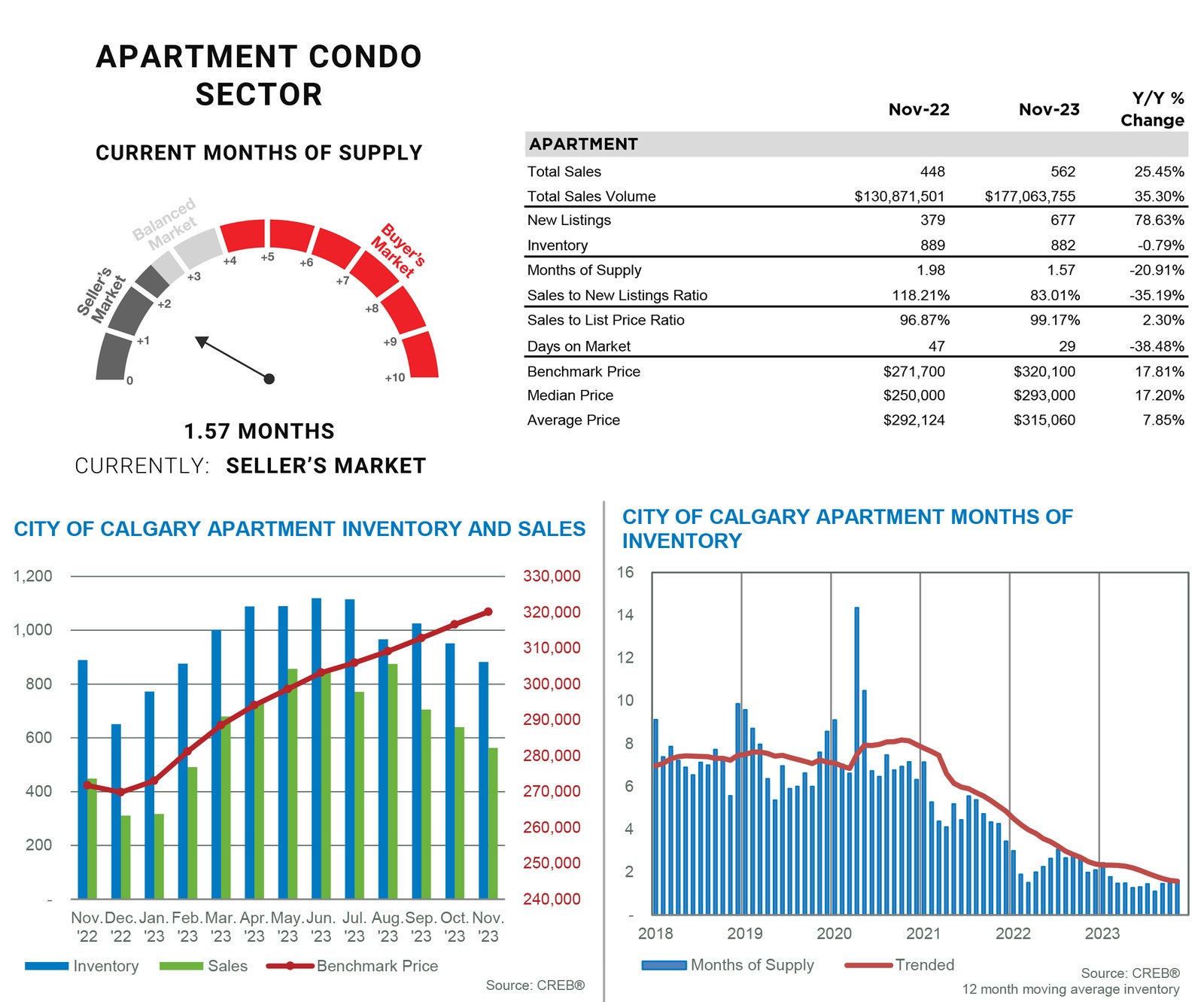

APARTMENT SECTOR

Thanks to the relative affordability of the apartment-style homes, sales continued to reach record highs in November, contributing to year-to-date sales of 7,487. With one month left in the year, sales have already surpassed last year’s record high. This, in part, was possible thanks to the growth in new listings. While inventory levels are similar to levels reported last year, with less than two months of supply, conditions still favour the seller, placing further upward pressure on prices.

The unadjusted November benchmark price reached $320,100 in November, a monthly gain of over one percent and a year-over-year increase of 18 percent. Year-to-date price gains have occurred across every district in the city, with some of the largest gains arising in the lower-priced North East and East districts.